Refinance is an option to borrow money against equity in your home. For borrowers who have additional cash but are unable to pay the full amount, a home equity loan may be an option. Both have their benefits and drawbacks. Homeowners with equity can make a smart decision to refinance their cash-out loans. Although cash-out refinances are more affordable and easier to qualify for than other options, they can also be expensive.

Refinances with cash-out have lower interest rates

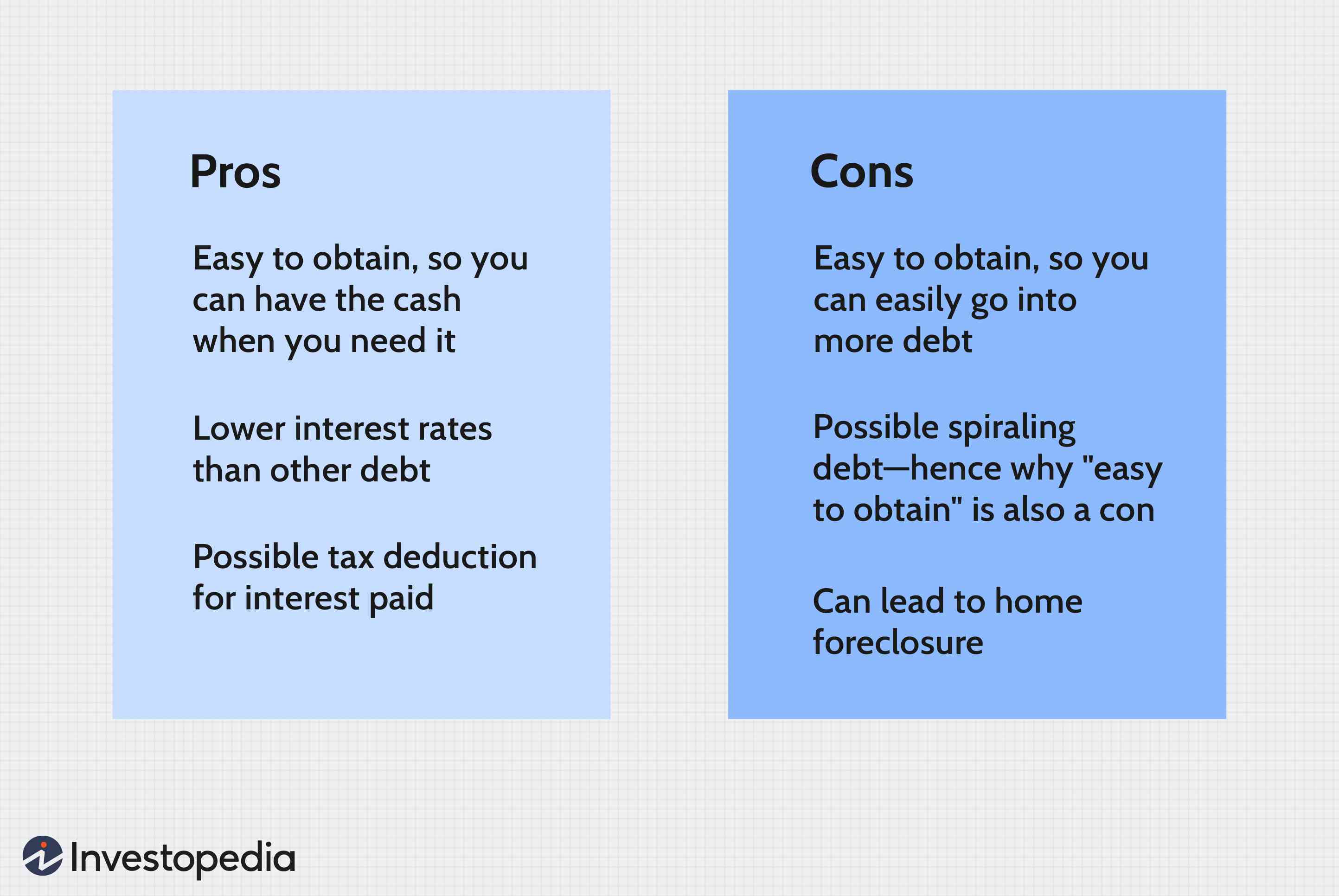

A cash-out refinance can be a good way to take advantage of the equity in your home without paying as much as you would on a home equity loan. However, you need to consider the drawbacks of such a loan. Cash-out refinances can make your mortgage more expensive, extend your repayment period, and even increase your risk of foreclosure.

While cash-out refinances usually have lower interest rates that home equity loans, you will still need to pay fees. The closing costs may be as high as 3% of the new mortgage balance. You will also have to pay homeowners insurance, property taxes, and other fees. You may find cash out refinances a great option if you have good credit.

It is easier to be eligible for them

A home equity loans allows homeowners to borrow against the equity in their homes. These loans have lower interest rates, and are easier to obtain than a mortgage refinance. Home equity loans may have lower closing costs and be more flexible that traditional mortgages. You should be aware of the requirements before you apply to a home Equity loan.

You can borrow against the equity of your home, then pay it back in set amounts that include interest and other fees. This loan is also known by the name "second mortgage" because it borrows against your home and then pays back in a set amount of installments, which includes interest and fees. If you default on the loan the lender can foreclose your home. While refinancing is more common than a mortgage to fund your home equity, it's important to evaluate all factors before choosing a loan.

They are more convenient

A home equity mortgage might be an option for you if your credit is good and you have a lot of equity in the home. Cash-out refinances are a good option for those who only need to lower their monthly mortgage payment. Consider getting multiple quotes from different lenders before making a decision. A detailed list of fees for lending should be requested.

Refinances are loans that replace your existing mortgage. A home equity mortgage, on the other side, is a second loan which you take out in addition to your current mortgage. Both have their pros and cons. Before you decide which one is best for your needs, it is important that you fully understand the risks associated with each.

They come at a higher price

Refinance loans can help you save money over the long-term because you can release equity in your home. Refinance loans are more expensive upfront but will have lower monthly payments than home equity loans. However, if you plan on paying off your loan within six months or less, a home equity loan will be more affordable.

It is easier to get a home equity loan. However, it will also require you to pay closing costs. These costs are typically not tax-deductible. The flexibility of a home equity loans is another benefit. The money can be used to pay for major purchases and other expenses.

FAQ

How can I determine if my home is worth it?

You may have an asking price too low because your home was not priced correctly. You may not get enough interest in the home if your asking price is lower than the market value. For more information on current market conditions, download our Home Value Report.

How long does it take to get a mortgage approved?

It depends on many factors like credit score, income, type of loan, etc. It takes approximately 30 days to get a mortgage approved.

What time does it take to get my home sold?

It all depends on several factors such as the condition of your house, the number and availability of comparable homes for sale in your area, the demand for your type of home, local housing market conditions, and so forth. It can take from 7 days up to 90 days depending on these variables.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to become a real estate broker

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

Next you must pass a qualifying exam to test your knowledge. This requires studying for at minimum 2 hours per night over a 3 month period.

You are now ready to take your final exam. For you to be eligible as a real-estate agent, you need to score at least 80 percent.

You are now eligible to work as a real-estate agent if you have passed all of these exams!