One of the most common misconceptions about short sales is that it is all about selling the home. But the truth is much more complex than that. The process involves both a borrower and the house. Understanding both is crucial to a successful short sale transaction. Here are some points you should keep in mind.

Short sale purchase

A short sale is a great way of getting a great deal on your home. This is a more difficult option than buying a house. You'll first have to prove to the lender that your income is not sufficient to pay the mortgage. You can do so by presenting a hardship notice and proof that you have income. Another important document is your CMA, which aggregates home sales and estimates the current value of your house.

A few things you should be aware of when purchasing a short-sale home. For example, a short sale home will typically have more problems than a normal home. The sellers may not have the money to fix their home. Sometimes they are emotionally upset and will take their anger out on the home. Buying a short sale home may be the best option for you if you're not interested in a huge amount of repairs.

In a short sale, the lender's role

A short-sale lender's role is helping a homeowner to sell their home for less that the remaining loan balance. A short sale allows the homeowner to pay less of the loan amount and the bank will keep the rest. A short-sale process can take months to complete. The lender will not tell the homeowner how much it wants to sell the home for, but will look at what a buyer offers and then decide whether or not to accept it.

Once a lender agrees to entertain a short-sale, the next step is to contact the lender's loss mitigation department to apply for short-sale approval. Make sure you speak to the same person every time you call. Be sure to explain your situation and provide copies of any relevant documents, such as a termination letter and medical bills.

Short sale loans

If you're interested in purchasing a short sale property you might consider applying for a loan to finance it. Short sale loans are more complicated than traditional mortgages, and take longer approval processes. Lenders typically lock in the interest for two months after the sale has been approved. This could mean that depending on the lender you might have to wait several weeks, or even months, to close your loan.

The first step in getting a short sale loan is to explain your financial situation to the lender. You'll need to show proof of your inability to make payments on your current mortgage. Your lender will usually consider how much income you have and the amount of your debt. Your chances of approval are higher if you can reduce your debt significantly.

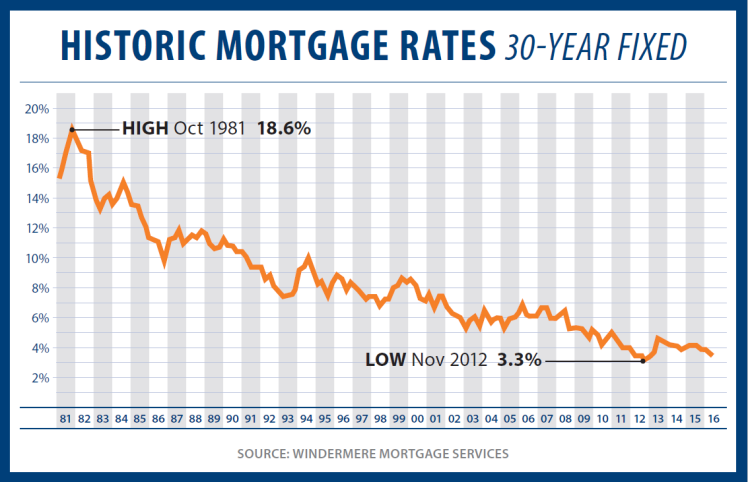

FAQ

What are the benefits associated with a fixed mortgage rate?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This will ensure that there are no rising interest rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

What are the disadvantages of a fixed-rate mortgage?

Fixed-rate mortgages tend to have higher initial costs than adjustable rate mortgages. You may also lose a lot if your house is sold before the term ends.

Should I rent or purchase a condo?

Renting may be a better option if you only plan to stay in your condo a few months. Renting lets you save on maintenance fees as well as other monthly fees. The condo you buy gives you the right to use the unit. You can use the space as you see fit.

How much does it cost to replace windows?

Replacing windows costs between $1,500-$3,000 per window. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

How much money do I need to save before buying a home?

It depends on the length of your stay. It is important to start saving as soon as you can if you intend to stay there for more than five years. But if you are planning to move after just two years, then you don't have to worry too much about it.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to Purchase a Mobile Home

Mobile homes are houses that are built on wheels and tow behind one or more vehicles. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. People who want to live outside of the city are now using mobile homes. Mobile homes come in many styles and sizes. Some houses are small while others can hold multiple families. You can even find some that are just for pets!

There are two main types for mobile homes. The first type is manufactured at factories where workers assemble them piece by piece. This happens before the product can be delivered to the customer. Another option is to build your own mobile home yourself. Decide the size and features you require. You'll also need to make sure that you have enough materials to construct your house. To build your new home, you will need permits.

Three things are important to remember when purchasing a mobile house. Because you won't always be able to access a garage, you might consider choosing a model with more space. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. The trailer's condition is another important consideration. Problems later could arise if any part of your frame is damaged.

Before you decide to buy a mobile-home, it is important that you know what your budget is. It is important to compare the prices of different models and manufacturers. Also, consider the condition the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

A mobile home can be rented instead of purchased. Renting allows you to test drive a particular model without making a commitment. Renting isn’t cheap. Most renters pay around $300 per month.